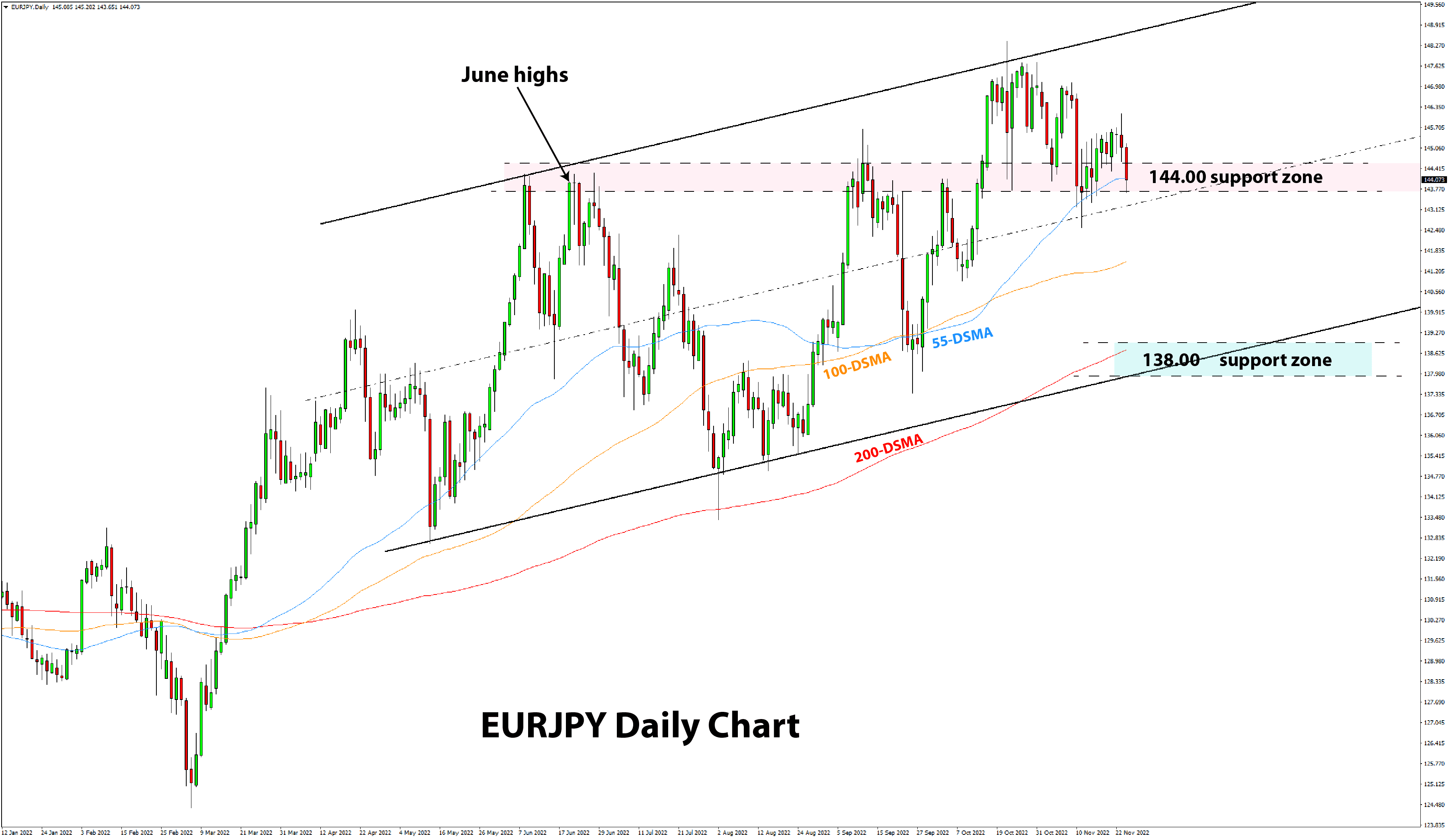

On the fundamentals side, things remain little changed from six months ago. Back then, we said, “the market expects too much from the ECB and too little from the BOJ”. Indeed, with the EURJPY exchange rate

almost unchanged since our June 23 newsletter, that premise has largely been proven correct, although not to the extent that EURJPY would move lower.

Nonetheless, as of the moment, there is no hawkish pivot from the Bank of Japan. This is certainly keeping upward pressures intact on JPY pairs, including EURJPY. Yes, the euro is very weak this year, but the Japanese yen has been weaker because the BOJ

“out-doved” every other central bank.

However, the time may not be far

when the BOJ will have to join the “pivot” camp. Already last week, Japan’s national core CPI inflation surprised higher. This week (Tue), the BOJ core CPI y/y also surprised notably higher at 2.7% actual vs 2.2% forecasts. Remember, Japan has a number of different CPI inflation measures like these that the BOJ tracks and takes into account when setting

policy. Another CPI report is due on Friday (the Tokyo Core CPI y/y).

While Japan’s economic reports usually don’t move the market, they are watched by the BOJ and have an impact on their policy. The point is inflation in Japan is now rising clearly above the 2% target, which could mean the BOJ won’t be able to stay uber-dovish forever.

Another aspect that could be turning more favorable for the yen from here is that inflation in the US and Eurozone may be close to peaking or may have already peaked. Eventually, this would mean lower bond yields in the EU and the US, which would be bearish JPY pairs just as it was bullish when yields were rising earlier this

year.

So, multiple factors may be slowly aligning for a turn in the

tides of JPY. Still, as we said back in June, a short EURJPY is likely to be a better play (safer trade) compared to a short USDJPY simply because the EUR fundamentals are still weaker compared to the USD.

If you follow our regular weekly Fx analysis published every Monday, you know that we

expect EURUSD to eventually revisit the parity area (1.00) and even drop below it, perhaps even before the Christmas season. In line with this, shorting the EUR is the preferable option.