EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(June 27 – July 04, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains a short preview of the article.

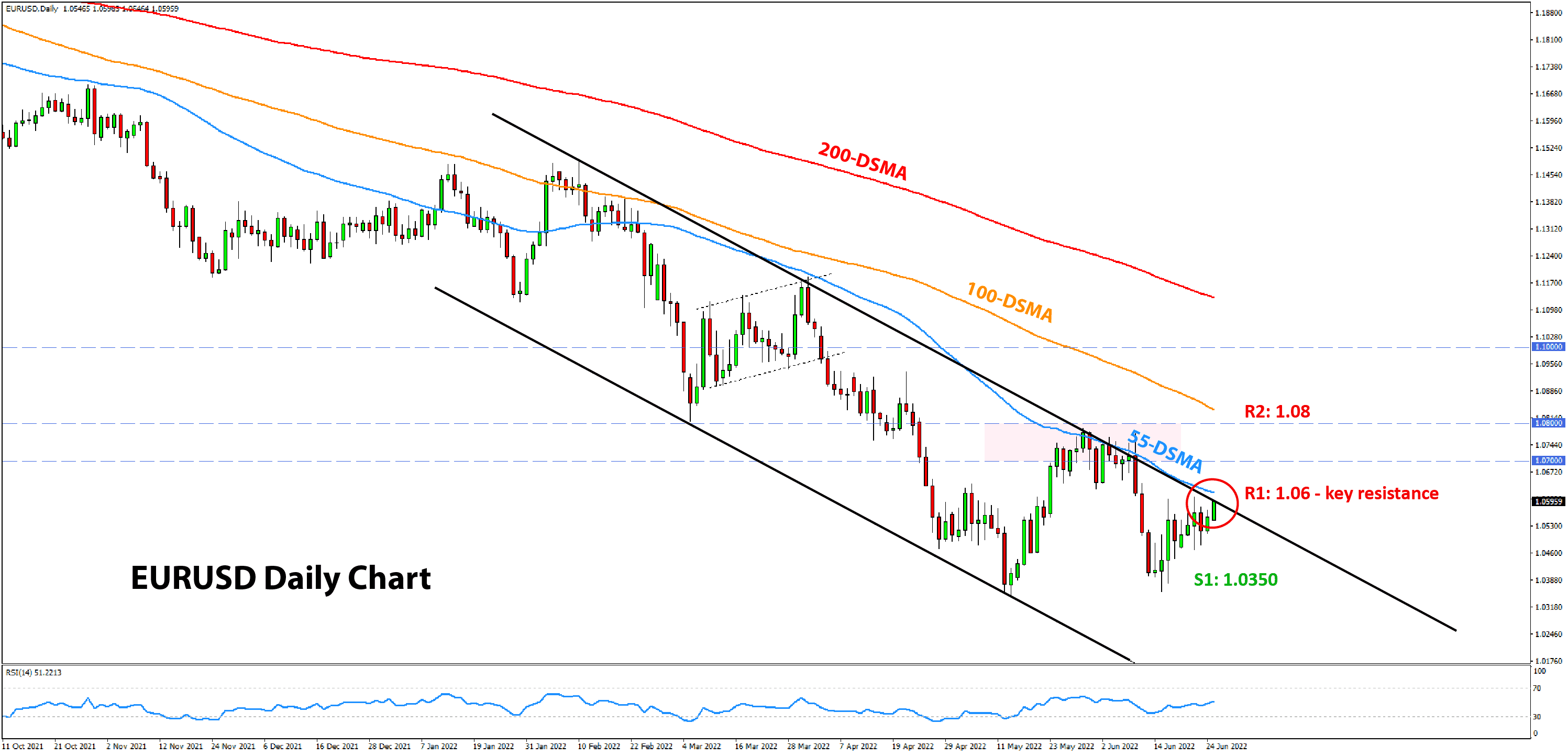

EURUSD Technical Analysis

EURUSD is still trading inside of the downtrend channel that started in February but is making another test at the trend’s resistance line today. The trendline resistance is currently located at the 1.06 zone on the daily chart. The still strong momentum of the bears suggests a bullish breakout is unlikely to come easily here.

In any case, if a break above 1.06 happens, the next resistance is at the prior highs around 1.08. In such a case, EURUSD will need to be looked at within the larger context (weekly/monthly charts). But those are also in a bear trend that started with the highs from one year ago (May 2021).

To the downside, support is now solidly standing at the 1.0350 zone. The 1.05 level will remain an important technical point on the charts if EURUSD starts moving down again.

USD Weekly Fundamental Outlook: Has Inflation Peaked? Dollar Consolidation May Extend as Bond Yields Fall

The dollar continued to consolidate lower over the past week, driven mostly by sharp moves in other markets, while Fx action remained subdued. While a few days ago, everyone feared inflation, a series of bad leading indicators (PMI reports) from developed economies and falling commodity prices turned this around, with many now questioning if we might be near the peak of inflation.

The large drop in commodity prices (including oil) helped to relieve inflation fears, and the focus has turned to the risks of an incoming global recession. If inflation is really peaking here, it will have significant implications for central banks. They will likely not need to tighten and hike rates as aggressively as currently anticipated. The Fed would probably also tone down its hawkish stance in such a scenario. The markets already adjusted rate hike expectations lower last week, which is the reason behind the extension of the USD correction and the fall in bond yields.

But, it’s not just Fed rate hike expectations that declined but for all other central banks too. So, while peaking inflation might mean some of the trends in global markets will reverse, in Fx the US dollar still stands to gain on two pillars in the months ahead – via the yield differential factor (higher rates than other countries) and via the safe-haven factor given the overall risk-off tone in markets this year. Both of these are

unlikely to change soon, regardless of whether the Fed proceeds with the aggressively hawkish plans or dials down a bit.

Ultimately, the better-performing US economy and the country’s energy independence are the two fundamental bullish USD factors. This is what allows the Fed to be more hawkish than other central banks and deliver more aggressive rate hikes. So, even if the Fed turns less hawkish in case inflation has peaked, other central banks would likely turn even more dovish in such a scenario. Therefore, the US dollar should still largely remain a

winner.

On the calendar, PCE inflation (Thur) and the ISM manufacturing (Fri) will grab the main attention. High inflation prints and above estimates numbers in the ISM manufacturing should prove USD bullish again, while a miss may extend the dollar correction. There will be several Fed speakers throughout the week (including Powell) as well as other economic data like consumer confidence and final GDP. Overall, depending on the outcome of these

events, the USD may extend the correction lower, particularly if inflation fears further abate this week, e.g., via further decline in commodities or lower (US) PCE and (Eurozone) CPI inflation readings.

EUR Weekly Fundamental Outlook: Euro Stabilizes, but Recession Risks Mean Bearish Pressures Will Likely Resume Soon

The Eurozone manufacturing and services PMI reports released last Thursday were all dismal, missing expectations by wide margins. This confirms the negative outlook for the economy in the face of the Russo-Ukrainian war. Furthermore, the recent sharp increase in European gas prices (TTF futures contract) as Russia further cuts supplies is another fresh negative for the EUR currency.

Yet, the euro held up last week, though largely due to external factors. In an overall wild action in bond and commodity markets, Fx took a back seat, allowing for some consolidation to transpire. However, the already established Fx trends are unlikely to change soon, with the bearish dynamics for the EUR currency remaining fully intact. A recession in the Eurozone later this year now looks like the probable scenario, with economic fundamentals much

weaker than peer economies due to Europe’s reliance on energy imports. With Russia unlikely to increase gas flows any time soon, prices remain high and will keep weighing on the economy.

The focus on the economic calendar this week is CPI inflation. CPI reports from various EU member states will start rolling in from Wednesday, while the main attention will go to the aggregate CPI inflation report for the whole Eurozone due on Friday. However, traders need to particularly watch the German and French CPI reports, which are released on Wednesday and Thursday and may have an

early impact on the market.

Markets will also focus on the annual central banking forum in Sintra Portugal that starts today and will last until Wednesday. There will be many speakers, including Fed chair Powell, ECB’s Lagarde and BOE’s Governor Bailey. The markets will listen closely as central bankers may use this opportunity to hint at important policy changes (they’ve done so in past years). Nonetheless, if they

don’t announce anything big, we will likely see only muted market action.

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders or tabs (often in the promotions tab). To ensure that all trade

signals I send will end up in your (primary) inbox folder you can add my email address to your contacts list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

|

|

|

|