EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(June 20 – June 27, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains a short preview of the article.

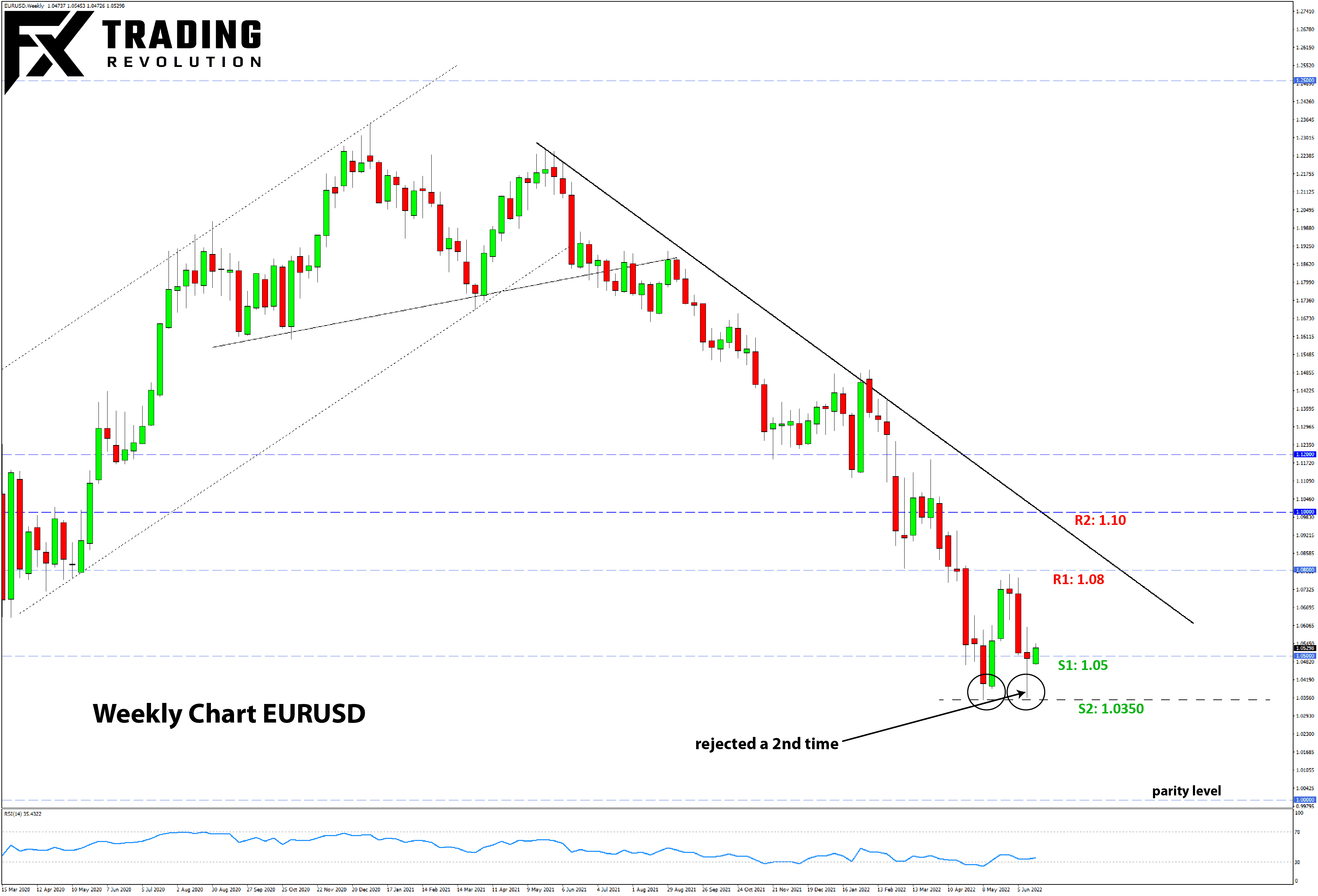

EURUSD Technical Analysis

EURUSD closed the past week with a high wave candle, indicating market indecision at the current juncture. Interestingly, the close was above the 1.05 level, while the weekly low was at the 1.0350 support zone. Based on this, we can say that the 1.0350 support zone has been solidified, which suggests a potential for the consolidation that started in early May (previous

low) to be prolonged for a while more.

That being said, the powerful bearish momentum has hardly been challenged at all. EURUSD remains inside the strong downtrend, with strong resistance zones at 1.08 and 1.10 keeping the trend intact. If the consolidation is prolonged, any rally will likely have a hard time breaking through either 1.08 or 1.10.

On the other hand, a break below the 1.0350 low in the near term would signal the trend is ready to continue without a lengthier consolidation. In this case, all focus will shift to the parity zone (1.00) as the next important support for EURUSD.

USD Weekly Fundamental Outlook: Fed Turns More Forcefully Hawkish, Dollar to Stay Bid

Central banks ruffled the markets last week, with the Fed, ECB, and SNB all delivering major surprise decisions. Naturally, this spurred wild swings across the Forex and other markets. As usual. the US dollar was at the center of the action, though the largest surprise was perhaps from the Swiss central bank (SNB), which shocked everyone with a 50bp rate hike. The Swiss franc strengthened sharply after their announcement.

In the US, the Fed also delivered a surprise of a larger 75 bp hike (50bp was expected). This was interpreted as an attempt for the FOMC to show its seriousness in fighting inflation. The forward guidance in the dot plot and communication by Powell during the press conference suggest that even the risk of a recession will not deter them from its hawkish trajectory. Inflation is now enemy no. 1, and the

Fed will do everything to bring it down to the 2% target.

Aside from the wild gyrations and dollar correction last week, the long-term bullish factors for the US dollar remain largely unchanged. The US economy is (still) in an advantageous position compared to others (especially Europe) which will allow the Fed to be and probably stay more hawkish than the ECB and others this year. Furthermore, Fed tightening is bad for risk-sensitive assets, increasing the odds that we will see more risk-off

episodes across different markets. This slight risk-averse tone in the markets can provide an additional boost to the safe-haven dollar. Thus, the USD stands to benefit from two factors this year - via the yield differential channel (higher rates than others) and via the safe-haven channel in times of falling stock markets.

The calendar is relatively light this week. Today (Mon) is a holiday, and the rest is mostly filled with 2nd tier data like housing and consumer sentiment reports. The markets will instead likely place more attention on scheduled Fed speakers. Of those, Chair Powell’s two-day testimony before Congress on Wednesday and Thursday is the main event.

EUR Weekly Fundamental Outlook: ECB Emergency Meeting Helps to Calm Italian and Greek Bond Markets

The ECB held an emergency policy meeting only one week after their regular meeting, which is very uncommon. Yet, they didn’t announce anything big, other than plans to deal with fragmentation risks (i.e. borrowing costs rising much faster for Italy than for Germany). Nonetheless, even this announcement that they plan to do something seems to have done the trick (for now), and Italian and Greek bond markets

calmed down. This seems to have also helped the euro and kept it inside the consolidation versus the dollar.

Still, prospects that EUR strength can last remain grim at best. Yes, the ECB can artificially bring stability in Italian and Greek bond markets, but that will be done via QE purchases. This could have the effect of negating their planned rate hikes (to begin in July). Thus, the EUR will not be able to benefit from the ECB’s rate hikes to the same degree as other currencies can from their central

bank’s tightening. This dynamic will likely leave the euro vulnerable to prolonged weakness during the summer months, perhaps even longer.

The EUR economic calendar features flash manufacturing and services PMI data (Thur) and the German Io business climate index. Negative surprises in those could exert renewed bearish pressures on the EUR currency. Markets will also continue to monitor ECB communication, with several ECB speakers scheduled this week, including speeches by President Lagarde and Chief Economist Lane.

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders or tabs (often in the promotions tab). To ensure that all trade

signals I send will end up in your (primary) inbox folder you can add my email address to your contacts list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

|

|

|

|