EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(February 21 – February 28, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains only a short preview.

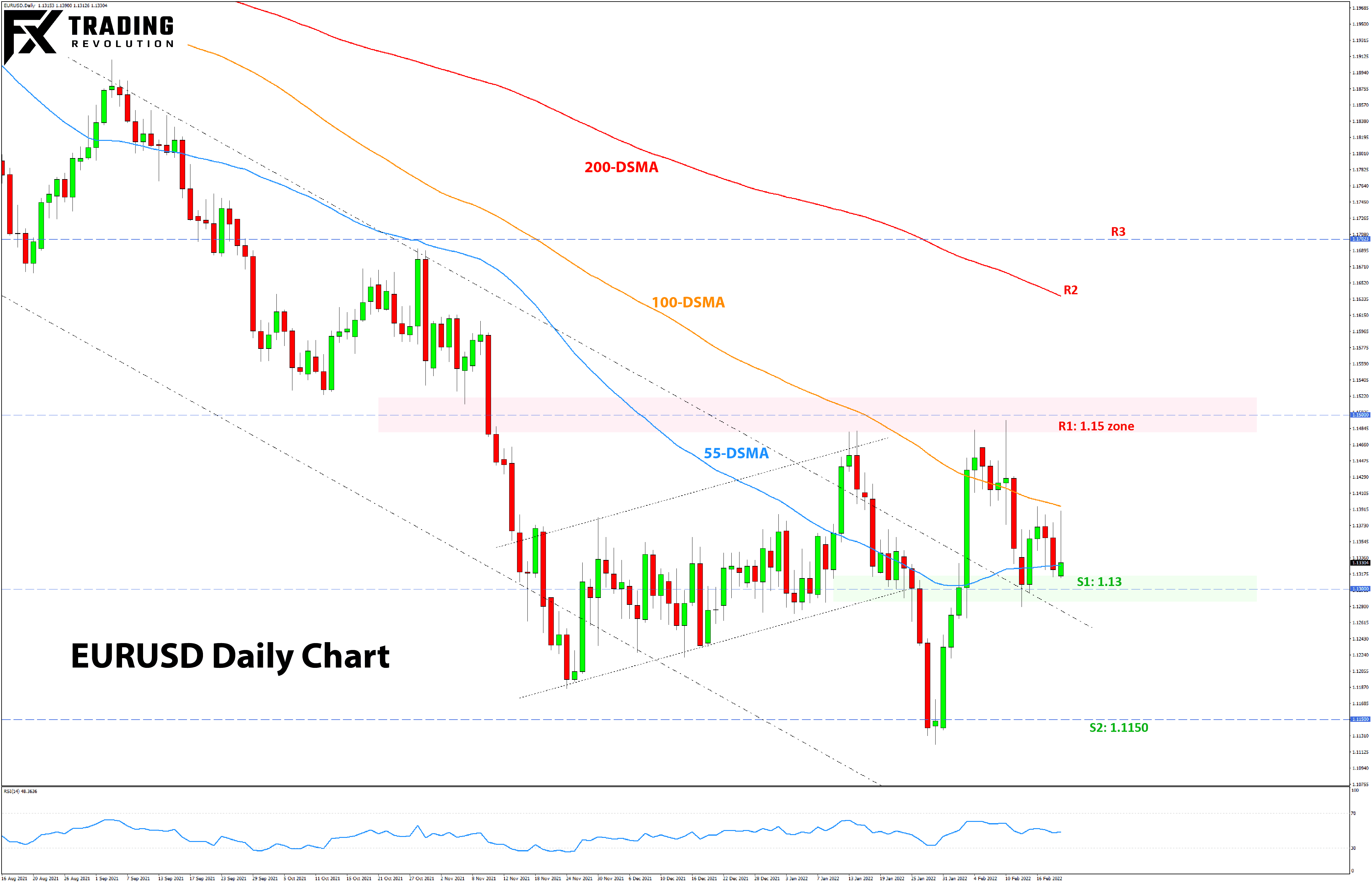

EURUSD Technical Analysis:

EURUSD was contained between the 1.13 and 1.14 zones over the past week, indicating that support and resistance zones may be establishing here. While the pair may stay capped between those two zones this week too, such a

range of 100 pips is very tight and rarely can hold for more than a few weeks.

That being said, the next key resistance higher is at the 1.15 zone. This is the more critical technical zone, and thus even if EURUSD moves above 1.14, the bulls will not get too excited as long as the exchange rate stays below 1.15.

To the downside, below the nearest 1.13 support zone, there is support at 1.1250 (modest) and the low at 1.1150, which is somewhat more significant. The next support lower is at the historically crucial 1.10 area.

Low spreads from 0.0 pips** ; No dealing desk and no requotes

Globally regulated; Segregated Client Funds

US Dollar Fundamental Outlook: Multiple Uncertainties & Russia-Ukraine Tensions Likely to Keep USD Rangebound

Following the volatile price gyrations in the first half of February, the market action last week was much more contained. Yet, the stabilization doesn’t come because anything has actually “stabilized,” but rather is more a reflection of market participants staying away from accumulating large positions due to the many uncertainties that

currently cloud the markets.

The Russia-Ukraine tensions, for example, were front and center last week, pushing markets up and down, even as the situation remains in “deadlock” mode (with neither escalation nor de-escalation). Although the moves were relatively modest, safe-havens were bought and risk-sensitive currencies were sold on news headlines that “Russia is about to invade Ukraine.” Then it became

clear that this was not the case and the moves duly reversed.

The other uncertainties stem from the 40-year inflation highs in many developed countries, which has prompted their central banks to turn hawkish. This factor could lead to more volatility via the bond and stock markets over the coming days and weeks. In particular, the main risk is a big sell-off in stocks, which can be very negative for risk sentiment and trigger similar

risk-off moves in the Fx market.

Turning to the immediate USD outlook for this week, the established ranges seem unlikely to break. Risk sentiment improved early this (Monday) morning on reports that Presidents Vladimir Putin and Joe Biden have agreed to meet (date not specified yet). The news has eased the greatest fears of war for now because investors assume “the

Presidents agreeing to meet” means negotiations are still the primary method rather than military escalation. Ultimately, this means that the markets will be kept in ranges, as the status quo and the uncertainties remain largely unchanged.

The US economic calendar is light this week, with the markets only focusing on the (2nd preliminary) GDP number on Thursday and the PCE inflation figure on Friday. While both are important economic reports, they are unlikely to trigger a big USD reaction. On the geological front, the focus will be this Thursday on the meeting between the Russian and US foreign ministers Blinken and

Lavrov, which should come as a prelude to that potential Putin-Biden meeting sometime after that.

Euro Fundamental Outlook: Ukraine Worries & ECB’s Pushback Against Market Expectations Weigh on EUR

The EUR was generally weaker last week, though the losses were modest. The markets’ focus on the Ukraine-Russia tensions and more warlike rhetoric between the two sides there seems to be the reason for investors dumping the euro in recent days.

While few - if any - are expecting an outright war in Ukraine, traders are careful as they know that Russia-Ukraine escalations will be most harmful for the EUR currency due to the geographic proximity and close economic links (especially energy imports). This risk aversion factor is likely contributing to the EUR’s underperformance in the past two weeks and remains a big

uncertainty for the next few weeks.

In the meantime, the ECB continues to push back against the markets’ “too hawkish” expectations for them to tighten policy. ECB officials who spoke last week reiterated that removing accommodative monetary policy will be a very gradual process.

The EUR is likely to continue trading with a modest bearish tone pressured by Ukraine-related geopolitical risks and the scaling back of ECB’s hawkish bets. However, the risks are two-directional in the near term. In one scenario, the bearish pressures can significantly intensify if Ukraine-Russia tensions escalate in a big way. On the other hand, improvements on this front could see a

relief rally in EUR pairs.

The Eurozone calendar is also scant of any major releases or events, mainly featuring some business sentiment surveys. The PMI reports were already out this morning, while the German Ifo business climate index will be released tomorrow. However, given the unfriendly geopolitical backdrop, EUR traders will likely focus more on that Thursday Blinken-Lavrov meeting instead of any economic

report.

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders or tabs (often in the promotions tab). To ensure that all trade

signals I send will end up in your (primary) inbox folder you can add my email address to your contacts list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

|

|

|

|