EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(February 14 – February 21, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains only a short preview.

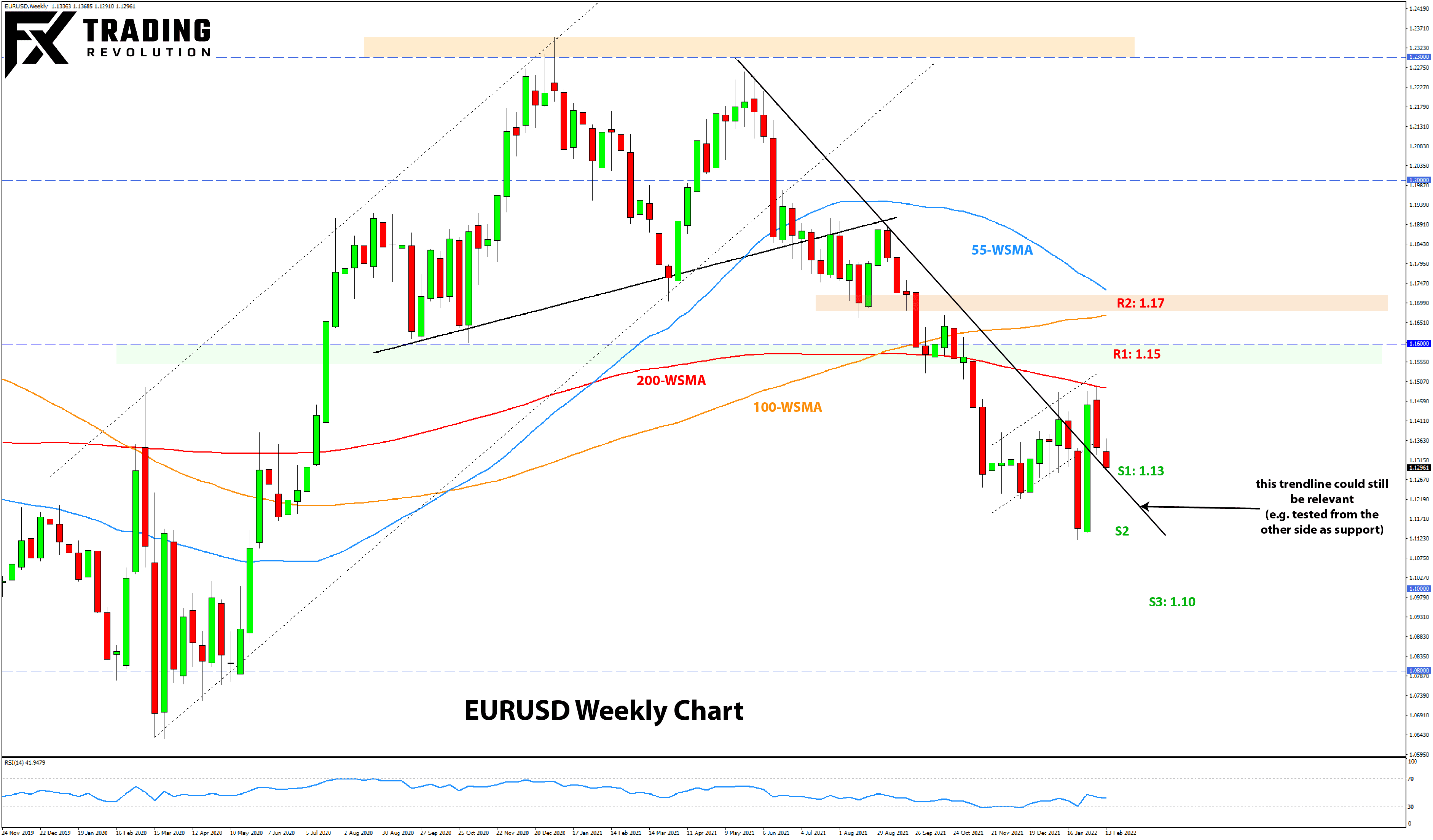

EURUSD Technical Analysis:

EURUSD stopped at the 200-week moving average just under the 1.15 level (actual 1.1491) and is now back below 1.14, even trading to 1.13 earlier today. This goes to show that while the bearish trend (channel formation) may have been broken, an uptrend doesn’t necessarily follow. At least not immediately it seems, and the rejection below 1.15 suggests (like the fundamentals) that range-trading is a probable scenario for EURUSD at this stage.

The key resistance to the upside remains at the 1.15 zone. Above it, perhaps even stronger resistance awaits in the 1.17 zone.

To the downside, 1.13 is an important support zone. Below it, there is support at 1.1250 and the low at 1.1150. Further down,1.10 comes into focus as the next major support area.

US Dollar Fundamental Outlook: Oh S**t, Inflation is at 7.5%, the Highest in 40 Years!

The highlight last week was the US CPI inflation report that surpassed consensus forecasts. The headline y/y CPI was 7.5%, while the core measure stood at an also high

6.0%! If it weren’t for Jerome Powell and Janet Yellen telling us it is all transitory, we would all be freaking out now.

Jokes aside, the markets also (for now) tend to believe inflation is transitory and that it will soon start to come down. Yet, that isn’t stopping them from pricing in an even more hawkish Fed in the coming months. Following that CPI inflation report last Thursday, Fed rate

hike odds in futures markets surged, now almost fully pricing (over 90%) a 50bp hike in March from around 30% before the CPI report. St. Louis Fed President James Bullard (voting FOMC member) was also speaking in favor of more drastic measures such as a larger 50bp rate hike and even an inter-meeting emergency hike, all helping to reinforce the hawkish Fed story.

It’s worth a reminder here that the Fed usually delivers what the markets expect it to do with a probability of above 60-70 percent. There is still time until the next meeting (March 16) – but unless those probabilities come down – the Fed will most likely deliver that 50bp hike. All of this “Fed hawkishness” is supportive for the US dollar, and as long as the Fed leads the hawkish “pack” among central banks, it will be hard for the other currencies to stand up against “king dollar.”

On the US calendar, Wednesday will be the busiest day, seeing the release of the retail sales report and then the FOMC minutes later in the day. Consumer spending is an important metric that the Fed

closely monitors, and a solid retail sales report should confirm the strength of the US economy. The FOMC minutes may provide more details about the Fed’s tightening plans, which likely means we can expect a bullish USD reaction, if any. Several FOMC members have speeches throughout the week, including Bullard again today and on Thursday. More Fed officials favoring a 50bp March hike or faster QT (quantitative

tightening) would likely refuel the USD’s bullish move.

Euro Fundamental Outlook: ECB Starts Pushback Against Markets’ (Too) Hawkish Speculations

In our previous weekly Fx edition (Feb 7), we said, “it’s questionable how sustainable the EUR rally based on a hawkish ECB can be in the months ahead.” It seems we didn’t have to wait too long for ECB officials

to start pushing back against the markets’ too aggressive pricing and expectations for ECB rate hikes. As a result, the EUR retraced some of its gains over the past week, and it seems more could follow this week (already happening today).

Nonetheless, nobody can deny the shift at the ECB from ultra-dovish to less dovish (or neutral). This is a big deal for the euro and will likely prevent material losses for the currency over the coming months (which would’ve been much more likely if the ECB stayed firmly in

the uber-dovish camp). However, the ECB will still lag most of the other central banks, so this “relative” dovishness should keep the euro pressured for the time being.

ECB President Christine Lagarde and chief economist Philip Lane spoke last week. Both stressed that the Eurozone’s inflation situation is different from other countries and is not accompanied by wage

growth. Indeed, Eurozone CPI levels are still lower than elsewhere and (importantly) are mainly driven by the rise in energy prices (oil and especially gas). This situation suggests that if energy prices start to fall, the ECB will likely be the first to abandon any hawkish plans as Eurozone inflation would start falling fast.

Given this dynamic of an “ECB talking about rate hikes but not actually serious about doing it”, it seems probable that the euro (and mainly the EURUSD pair) can draw out some broader range in the weeks ahead, especially going into that March 10 ECB meeting (where

they should provide more details about their recent policy stance changes).

The EUR calendar is light for this week. Of the most notable events, Lagarde and Lane will speak again, and the markets will surely listen closely. The German ZEW Economic Sentiment is due tomorrow (Tue).

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders or tabs (often in the promotions tab). To ensure that all trade signals I send will end up in your (primary) inbox folder you can add my email address to your contacts

list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

|

|

|

|