EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(April 04 – April 11, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains a short preview of the article.

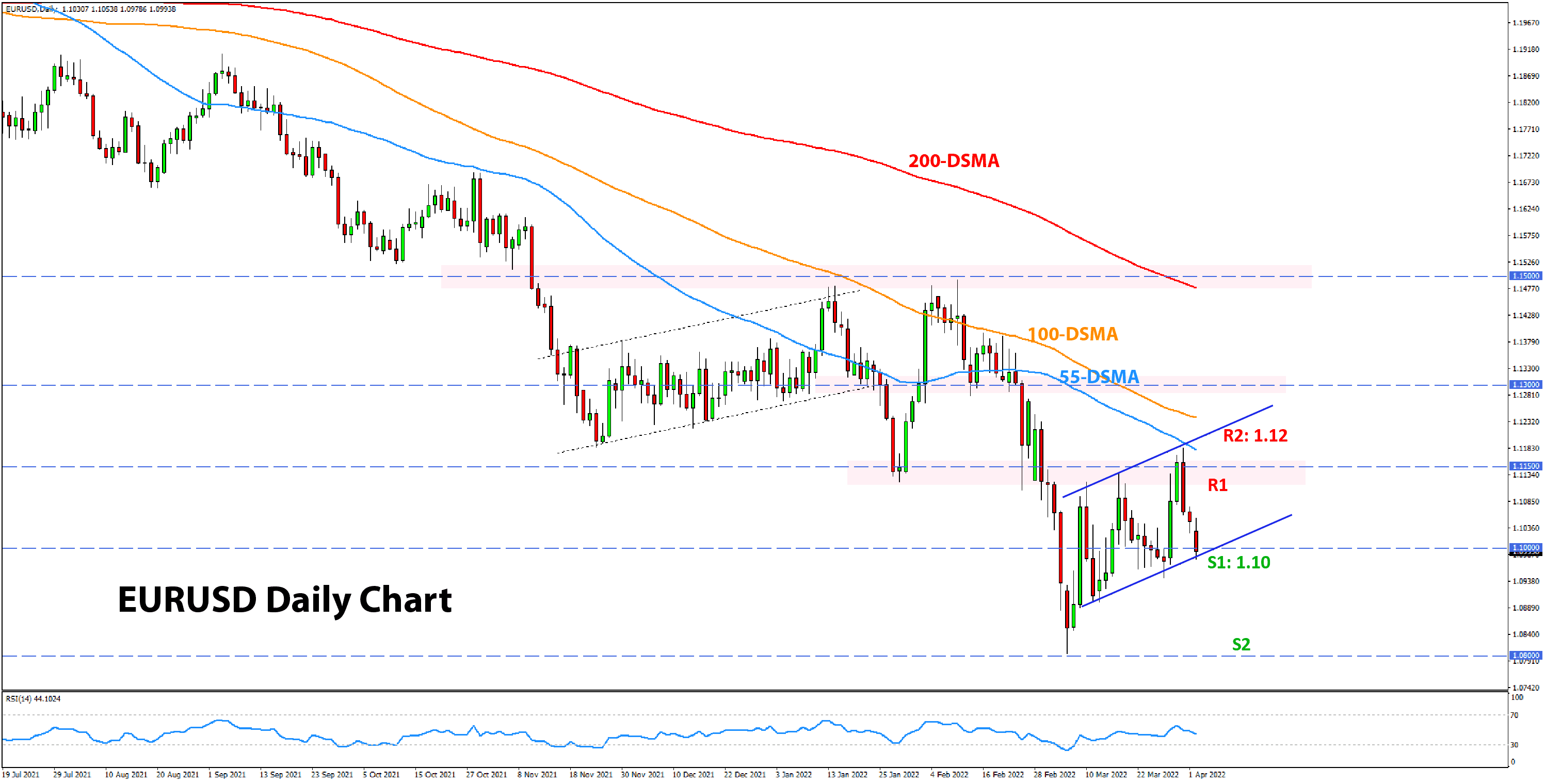

EURUSD Technical Analysis:

For this week, we turn to the shorter-term outlook on the daily chart, which shows a renewed attempt for EURUSD to break out of its consolidative range to the downside. For some context on the bigger picture (weekly chart), you can also check out the EURUSD technical analysis published last week.

The support line of the consolidative range comes in around the 1.10 level (chart below), with which the price is flirting today. A break to the downside will open the potential for a retest of the 1.08 low from early March. Before it, 1.09 will be a moderate support zone, though in this case, it’s likely to be less

significant following a break out of the consolidation.

To the upside, the first resistance on the daily chart would be at the 1.11 round number level. However, the more important resistance is located at the 1.12 area, where the previous highs/lows meet with the 55-day and 100-day moving averages.

USD Weekly Fundamental Outlook: Dollar Stays Firm, Albeit Still Inside Consolidative Range

The dollar stays generally supported, although it didn’t break to new cycle highs and is still trading inside its broader consolidation pattern that goes back to early March (i.e., DXY index). The solid jobs and NFP reports last Friday boosted hawkish expectations for more

potent Fed rate hikes, with futures markets now expecting two 50bp rate hikes in May and June (this would take Fed interest rates to 1.5% by summer already).

Other economic data from the US also supports the case for more aggressive Fed tightening. Inflation remains high while leading economic surveys such as the ISM PMIs remain at healthy levels. All this suggests that the Fed can be forcefully hawkish, if not for longer, at least in the next several months, before the rate hikes start to slow down the economy (perhaps Q4 2022). Thus, the

hawkish Fed, combined with the strong US economy in contrast to peers (mainly Europe), should continue to support the US dollar in the foreseeable future.

Still, given all this hawkishness, the dollar is only moderately strengthening so far, except for the faster appreciation against the weak Japanese yen. Again, this is a “healthy” reminder that Fx trading is a relative game. While the Fed is hawkish because inflation is high, so are other central banks (even the ECB) because inflation is high

everywhere. This is acting as a setback to larger USD gains at the moment; however, the weaker Eurozone economy should ultimately dampen any hawkish inspiration at the ECB in later months this year, which could keep the USD broadly strong for longer.

This week’s calendar is lighter, and the focus will go on the ISM services PMI survey (Tue) and the FOMC meeting minutes (Wed). Traders will watch the FOMC minutes for discussions around quantitative tightening (QT), where hawkish comments could fuel fresh bullish pressures on the USD.

EUR Weekly Fundamental Outlook: Ukraine Conflict De-Escalation, but Are Sanctions About To Be Stepped Up?

Some may find it strange that the euro is falling now that there has been some withdrawal of Russian troops on the ground in Ukraine (supposed military de-escalation). However, this all goes back to what we have discussed here in the past 4-5 weeks, which is that as long

sanctions remain in place, the euro will hardly be able to sustain any material gains.

And it now seems that even stronger sanctions from Western allies on Russia are on the cards, given the horrific images (of war crimes) that circulated in the media over the weekend. Russian gas and oil are still flowing to Europe, but a complete ban would mean that prices in Europe’s energy markets will go through the roof. This is a negative scenario for the EUR currency, and it’s

hard to see how Europe can lift sanctions on Russia, especially with the latest news of atrocities in Kyiv’s Bucha suburb. With the sanctions likely to remain in place (potentially permanently or as long as Putin is President), the immediate economic outlook for the Eurozone remains rather grim.

In the meantime, Eurozone economic data showed inflation continued to push higher while business sentiment surveys (PMIs) weakened further. This is all in line with the stagflationary environment, putting the ECB in a really tough spot over the next months of having to choose between fighting inflation or supporting economic growth. The odds are that the negative economic outlook will prevent the ECB from tightening policy as much as others (e.g., the Fed), thus continuing to exert downward pressure on the EUR currency.

The EUR calendar for this week is light, featuring only 2nd tier data like industrial production and retail sales. Fx traders also need to keep an eye on the French Presidential election on Sunday (Apr 10). While sitting President Emmanuel Macron is widely expected to win both rounds, surprises are always possible in politics, so some extra caution here can do no harm.

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders

or tabs (often in the promotions tab). To ensure that all trade signals I send will end up in your (primary) inbox folder you can add my email address to your contacts list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of

or reliance on such information.

|

|

|

|