EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(March 14 – March 21, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains only a short preview.

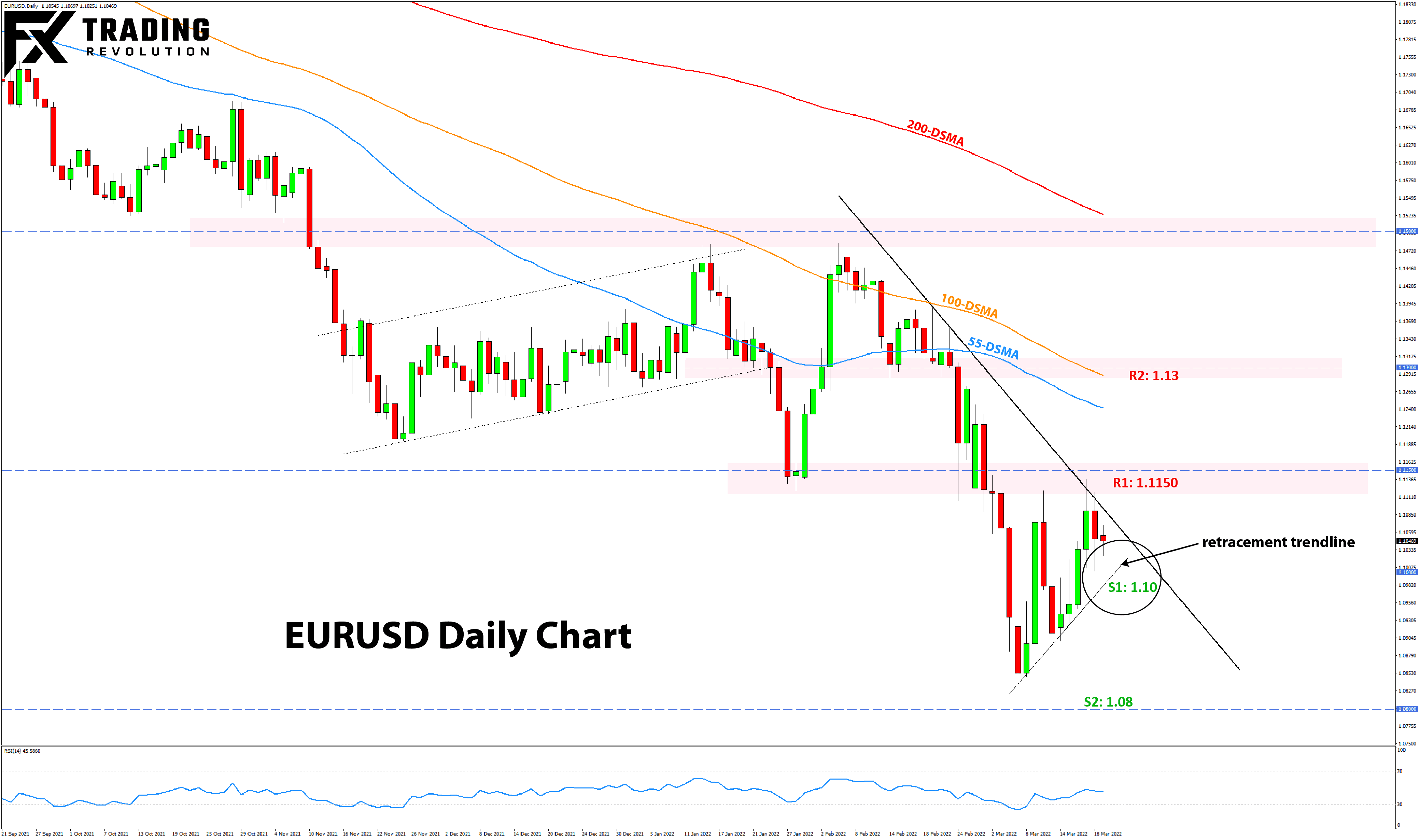

EURUSD Technical Analysis:

EURUSD climbed north of 1.10 again last Wednesday and has held above it. However, it couldn’t push through the important 1.1150 technical resistance. In fact, upon testing it, the bullish attempt was rejected. While another test is certainly possible, the rejection

on Friday shows that there is decent selling interest at levels above 1.11. Above 1.1150, the next resistance higher remains at 1.13. However, such a scenario would seriously threaten the current bearish trend.

The 1.10 level remains an important line in the sand. Notably, the rising retracement trendline seems to come near it also (see chart). This could mean that a break below 1.10 is the trigger signal for the next bearish leg in EURUSD. In addition, the pair is also trading below a

falling resistance trendline that last week stood near that same 1.1150 zone.

A break below 1.10 should signal that a revisit of the 1.08 area is becoming likely. Below it, the next round number levels of 1.07, 1.06, and 1.05 will be in focus as support zones. 1.05 is the most prominent one, which is also a critical technical support zone on weekly and monthly charts.

USD Weekly Fundamental Outlook: Fed Signals More Hawkish Rate Hike Path, Dollar Correction Looks Overdone

The USD’s consolidation continued, despite the more hawkish than expected Fed message last Wednesday. The dollar closed the week lower, driven by various counter-factors such as optimism on the war in Ukraine and general risk-on sentiment with a rebound in equity

markets.

However, as we’ve said here previously, even if a peace deal is reached today, the sanctions on Russia will (most likely) remain in place for a long time. The economic sanctions will continue to exert negative pressures on economies most closely linked to Russia, such as European countries, via higher commodity prices. This factor can keep the USD broadly supported in the

coming weeks and months, especially versus the most impacted European currencies.

Then, there is the possibility of a disappointment of recent hopes for a peace deal. The latest news from the ground in Ukraine do not suggest any lessening of hostilities, and both the Russian and Ukrainian sides haven’t signaled readiness to abandon some of their hard lines in the negotiations (a prerequisite for a peace deal). So,

have the markets gone too far pricing in Ukraine peace deal hopes? It certainly looks like so, and if a peace deal does not become a reality by Friday, we could already see last week’s moves reversed.

The Fed was much more hawkish than many anticipated, signaling more rate hikes ahead this year than economists expected. Chairman Powell also said QT (quantitative tightening) could begin as soon as the next meeting (May 4). Further, he confirmed that a more potent 50bp rate hike was discussed and definitely on the table for future meetings. Despite the lackluster initial USD

reaction, all this Fed hawkishness combined with the negative economic outlook for Europe and other countries points to more dollar strength in the weeks ahead.

The US calendar is not particularly busy this week, but there are a number of FOMC speakers, including Chairman Powell. Traders will focus on their comments around inflation, rate hikes, and quantitative tightening. Renewed hawkish discussions of 50bp rate hikes could potentially be another catalyst (in addition to the others above) for fresh USD gains this week.

EUR Weekly Fundamental Outlook: Euro Recovers on Ukraine Hopes, but Rally Unlikely to Be Sustained

The euro was one of the primary beneficiaries of the risk-on sentiment and optimism for a peace deal in Ukraine. But there is little to suggest the EUR’s gains (especially in EURUSD) are sustainable. With the war in Ukraine and the economic sanctions on Russia, the outlook for

the Eurozone economy is much grimmer than before. This crisis will definitely harm Eurozone GDP growth to a much greater degree than in other countries that are not as close to the war zone. Lower growth also means that the ECB (despite them trying to sound hawkish) cannot be as hawkish as other central banks whose economies are less impacted. Such central bank policy divergence in principle should lead to a weaker currency (EUR in this

case).

The negative impact from the war was already captured in the ZEW economic sentiment index last Tuesday, which plunged to -38.7 compared to a consensus forecast of a positive 10.3. This week, investors will look for similar evidence in the latest preliminary (flash) services and manufacturing PMI surveys (Thur) and the German Ifo business climate index (Fri), which are similar

leading measures of economic health in the euro area.

On balance, investors’ focus is likely to return to the negative growth outlook for Europe sooner or later, thus making the current EUR resilience look vulnerable to a reversal. Eventually, these dynamics should lead to a resumption of the EUR downward.

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders

or tabs (often in the promotions tab). To ensure that all trade signals I send will end up in your (primary) inbox folder you can add my email address to your contacts list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of

or reliance on such information.

|

|

|

|