EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(March 14 – March 21, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains only a short preview.

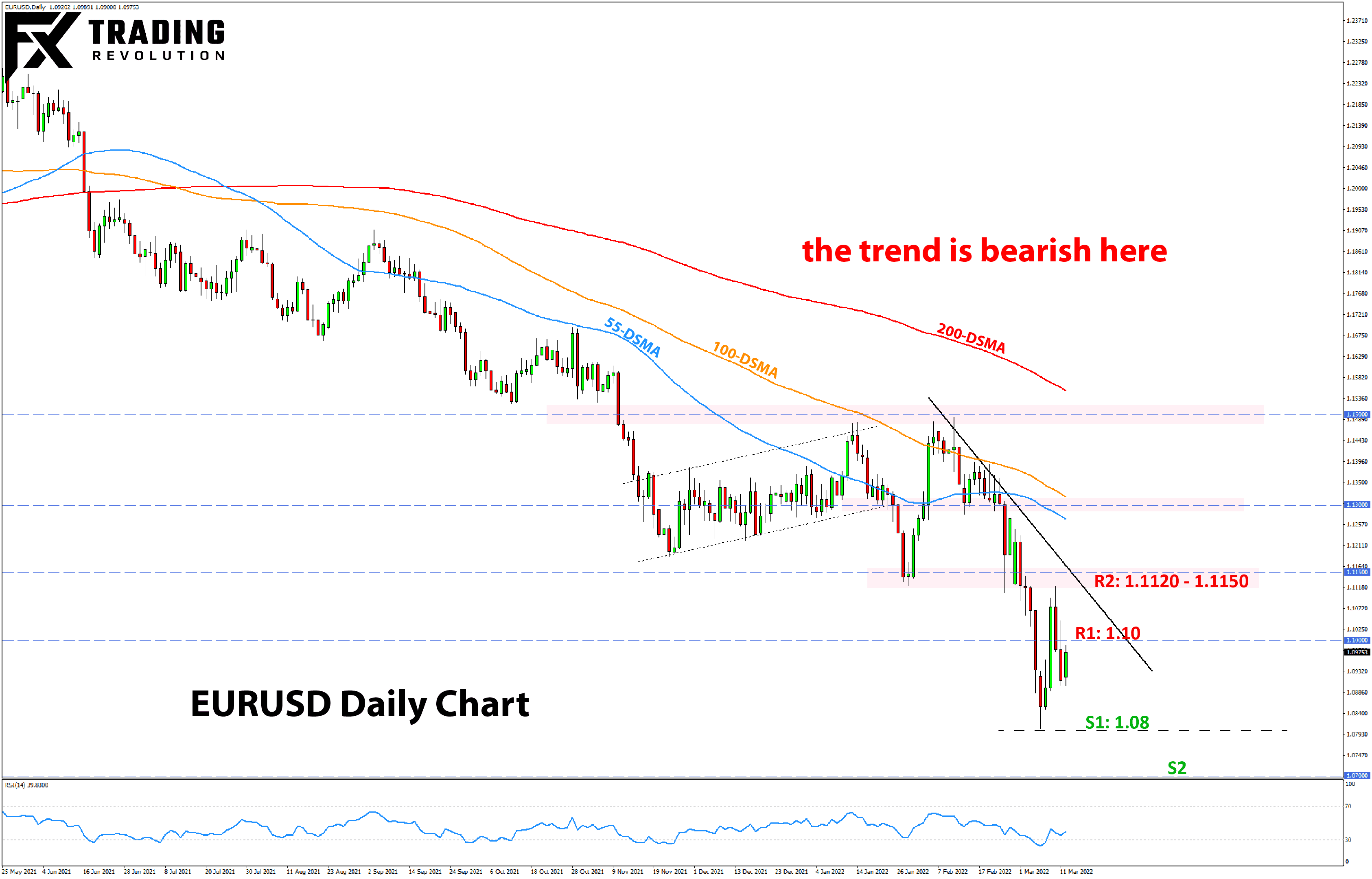

EURUSD Technical Analysis:

EURUSD has been in a steady decline since mid-February, with the bearish move accelerating following the Russian attack in Ukraine on February 24. After briefly testing the water above 1.10 last week, the pair is now back below this psychologically important level. The

1.10 mark can also be used as a proxy for near-term sentiment, meaning that when EURUSD is below it, sentiment is bearish.

The March 7 lows near 1.08 are now back in focus and may be attacked as soon as this week. A break lower could see a move down to the next round number levels of 1.07, 1.06, and 1.05. The 1.05 zone is the most prominent one, which is also a critical technical support zone on weekly and monthly charts.

To the upside, sentiment can shift bullish if EURUSD moves above 1.10 again. But that alone won’t be enough to turn the trend around. For that, EURUSD will need to break and hold above the 1.1120 – 1.1150 resistance zone. The next resistance would come at the 1.13 zone in such a scenario.

US Dollar Fundamental Outlook: Fed Hiking Cycle to Begin on Wednesday; USD Bull Trend Intact

Fx investors continue to prefer holding US dollars in the current environment of worrisome geopolitical relations between Russia and the West, aggravated by rising inflation and slowing economic growth globally. There is nothing on the horizon to suggest that these

dynamics will change soon, and thus the USD should continue to perform well.

The main focus this week is on the Fed meeting Wednesday. They’ve already well telegraphed that a rate hike is coming, and most likely a 25bp one. Based on recent FOMC communication and market pricing, the Fed is likely to deliver 6-7 further rate hikes this year, bringing the interest rate at or around 2% (now 0.25%). The

Fed’s hawkishness is fully justified by the strong recovery in the US economy and high inflation, now running at 7.9% y/y as last week’s CPI report showed.

There is potential for two-way volatility around Wednesday’s Fed meeting in the short-term, but ultimately, the direction for the dollar is likely to remain up. In this sense, the underperformance in European currencies against the USD should remain more pronounced than currencies that are geographically and economically more distant from the Russo-Ukrainian war.

On top of the hawkish Fed, risk aversion continues to be the dominant mood in markets given all the uncertainties at the moment (both geopolitical and inflation). That being the case, the US dollar stands to benefit from both factors. Risk aversion combined with a hawkish Fed creates a strongly bullish backdrop for the USD.

Traders will also keep an eye on other US data this week, like PPI inflation (Tue), retail sales (Wed), and Philly Fed manufacturing index (Thur).

Euro Fundamental Outlook: Even a Hawkish ECB Can’t Save EUR; EURUSD Can Fall Toward 1.05 & Beyond

The ECB surprised last week by outlining a more hawkish path for exiting QE this year than the markets expected. The EUR initially jumped on the announcement but fell steadily thereafter, erasing all the short-lived gains and beyond. EURUSD closed the past week significantly

lower off the 1.1120 high reached on the ECB’s announcement, indicating traders’ attention has returned to the geopolitical and economic risks from the war in Ukraine and the hostile relations with Russia.

This is no surprise as the outlook for the Eurozone economy is now much grimmer than before the war. More expensive fossil fuels and commodities will hurt the global growth outlook, but much more Europe’s due to the high dependence on Russian energy (especially gas). The sanctions on Russia will likely keep gas prices high in Europe for a prolonged time,

potentially leaving a lasting negative impact on the EU economy and thus permanently scar the EUR’s fundamental valuation. After all, paying for more expensive gas from now on means Europeans (i.e., businesses & consumers) will have less money to spend on everything else (lower GDP growth). Weaker GDP prospects imply that Europe will be a less attractive destination for investors than before

(hence money flowing out of Europe). In Fx language, this means that the odds for EURUSD to fall to 1.05 and even to parity (1.0) have now increased several folds.

The EUR calendar is much quieter this week, featuring the ZEW economic sentiment surveys tomorrow (Tue) and a speech by ECB President Lagarde (Thu). The negative outlook for the EU economy should already be reflected in the leading ZEW surveys, which are set to plunge at much lower levels compared to February (released before the war in Ukraine). The ZEW reports may act as a

catalyst for the next leg lower in EUR pairs.

News from Ukraine will continue to be closely watched by markets. Negotiations resulting in positive developments (like ceasefire) can provide a relief rally for EUR pairs, and perhaps this is the biggest risk in holding short EUR positions. Still, it’s unlikely that a ceasefire deal alone can provide lasting support, and thus any

EUR rallies based on such news should still be short-lived.

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders

or tabs (often in the promotions tab). To ensure that all trade signals I send will end up in your (primary) inbox folder you can add my email address to your contacts list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of

or reliance on such information.

|

|

|

|