US Dollar Fundamental Outlook: Shock 6.2% Inflation Rattles Markets, USD Goes Up!

Inflation was front and center for the dollar last week, and the much hotter than expected CPI report Wednesday helped to push the USD index to fresh highs for the year. The initial reaction was mixed, with inflation hedges like gold and silver rising and the USD even falling briefly, but then the USD started to rise again and closed the

day sharply higher.

Headline inflation was 6.2% vs. a 5.8% forecast, while the core CPI reading was also hot at 4.6% vs. 4.3% forecasted. The Fed’s confident “transitory” narrative is beginning to be seriously doubted, and there is a good chance that FOMC members will start to be more vocal in the period ahead. The

risks for a hawkish tilt at the Fed have just increased massively, and with that, the odds for a further rise in the USD. Following the post-CPI rally, the dollar was a tad weaker Friday on the huge miss in the UoM consumer sentiment survey. While an important report that the Fed watches closely, the weak UoM consumer sentiment should not sway the Fed to remain ultra dovish in the face of continued surging inflation.

The US calendar is relatively light for the week ahead, featuring the retail sales report and 2nd tier data such as housing and the Philly Fed manufacturing index. More interesting will be the array of Fed speakers throughout the week. The market’s overall takeaway from those little

speeches could very well end up being the main driver of the USD this week. With inflation already at 6.2% and no signs of it abating any time soon, many Fed speakers may lean on the hawkish side this week, which could provide another boost for the US dollar.

Another front to watch is President Biden’s expected announcement for the next Fed Chairman. He should make the call any day now, and while Jerome Powell is the most likely candidate to win the term (his 2nd), if he doesn’t, the Fx market could react by selling the dollar. Notably,

Lael Brainard is the other favorite candidate, and she is seen as a more dovish central banker. So, if she gets the term, the dollar could suffer initially on the announcement, albeit this too should be short-lived as who leads the Fed may not make a huge difference when inflation is at 6.2%!

Euro Fundamental Outlook: EU Countries Are Imposing Covid Lockdowns Again, Despite High Vaccination Rates. Yikes!

Covid lockdowns are here again in Europe, and people are not happy. Rightly or not, some European countries with relatively high vaccination rates (think Netherlands, Norway, Denmark) are still looking to impose restrictions on their citizens to fight a new surge in Covid cases and

hospitalizations. And we thought we would achieve herd immunity with vaccination rates of around 70% or higher. Disappointing!

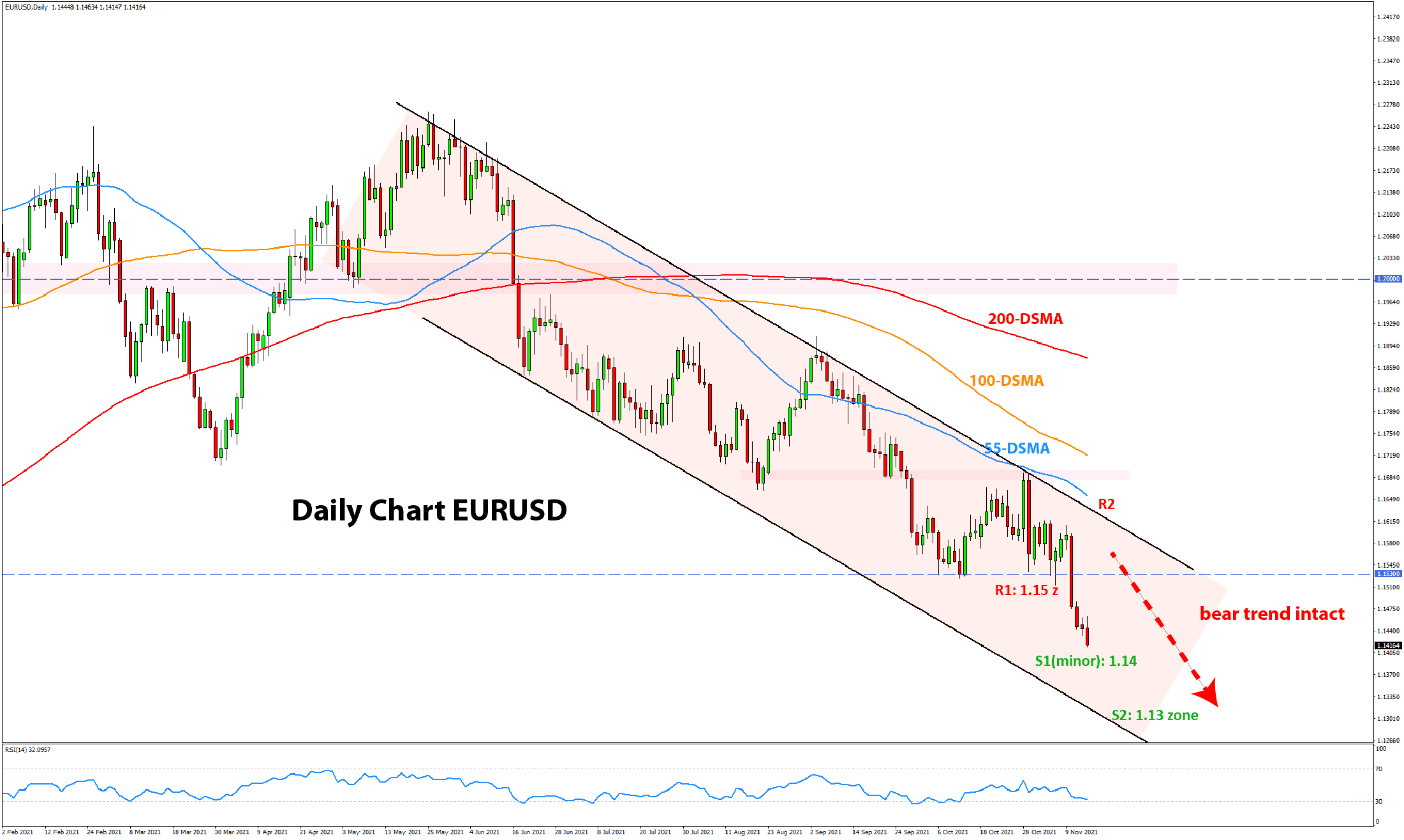

The euro doesn’t like the news either. The currency is breaking to new lows within the downtrend and was one of the worst performers in Fx last week. In the meantime, the economy should already be feeling the impact of the new Covid wave. The EU Commission forecasts released last week had similar inflation projections like the ECB, i.e., much lower than in the US and elsewhere. Thus, from this perspective, the main bearish EURUSD narrative of inflation and yields divergence between the EU and US remains in place and should continue to push EURUSD lower this and in the coming weeks.

This week’s Eurozone economic calendar is also light, with only the preliminary (flash) GDP scheduled for release tomorrow (November 16). If anything, a miss in expectations could only add to the EUR’s woes and push it further lower.