EUR/USD, GBP/USD, USD/JPY

Weekly Forex Analysis

(January 17 – January 24, 2022)

Hey! This is Philip with our new weekly outlook for EUR/USD, GBP/USD, and USD/JPY.

The text below contains only a short preview.

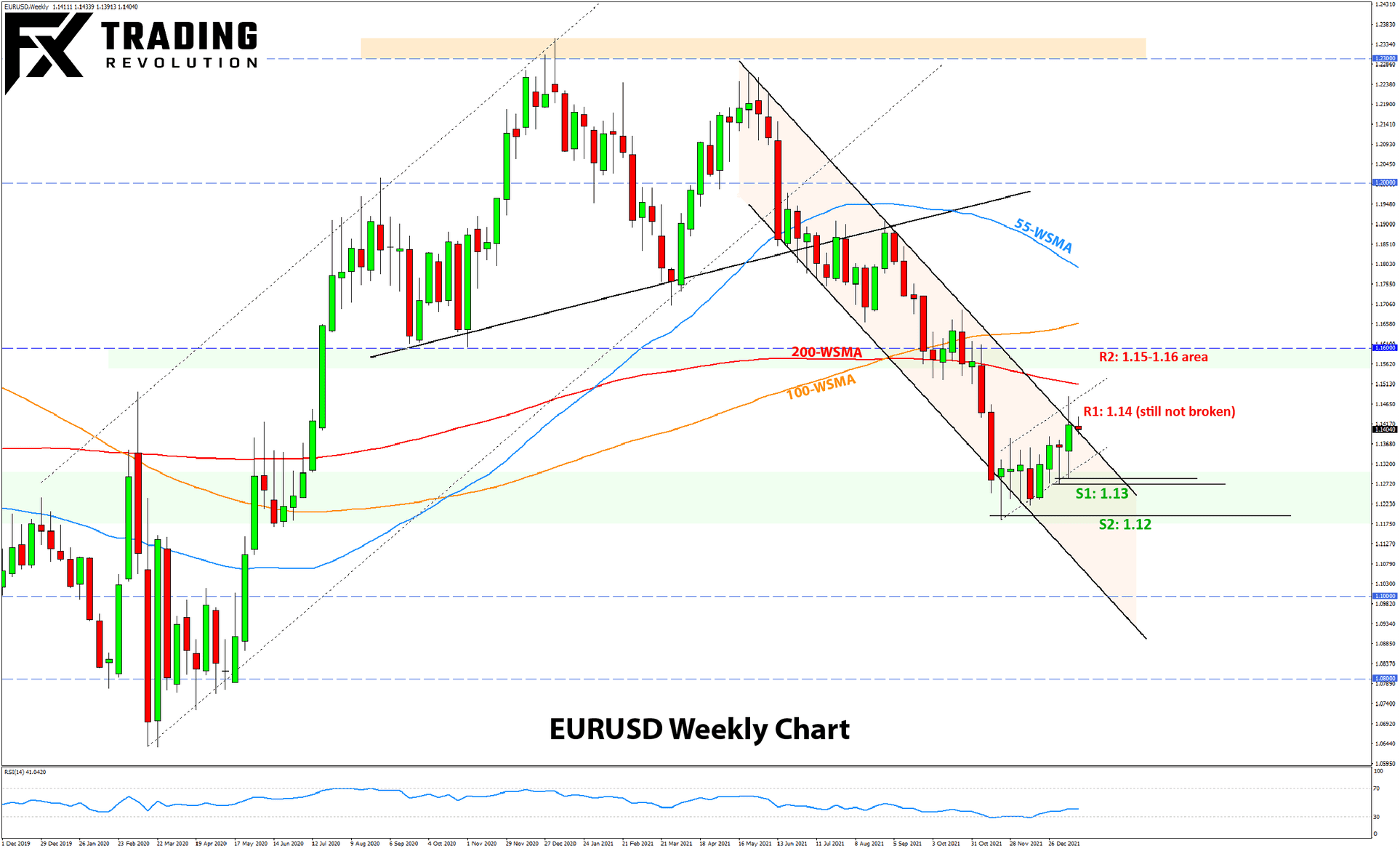

EURUSD Technical Analysis:

When looked from the daily chart, it appears EURUSD staged an upside breakout of the flag formation last week. However, a view at the weekly chart (shown below) tells that this breakout is far less convincing than the daily chart would make one believe.

The weekly chart indicates that the resistance trendline is not broken until a sustainable move above 1.14. EURUSD is testing exactly this zone at the moment. Another reason the breakout looks less convincing is that the upper border of the flag hasn’t been completely broken, despite the

move above 1.14.

As noted in the previous weekly edition, the 1.15 zone remains a key focus as resistance, particularly because of the cluster of technical zones aligning there, such as the moving averages (weekly-200 and daily-100) and prior lows.

Support to the downside is seen at 1.1350 and 1.1300, with the latter looking like a more significant zone because it represents the most recent prior swing low. A break below it would signal to the bears that a new bearish leg may be starting, which could accelerate the downside

action.

US Dollar Fundamental Outlook: 7.0% Y/Y Inflation Fails to Impress USD Bulls

The greenback extended its corrective decline before modesty rebounding on Friday to close the week off the lows. This was despite the US CPI inflation report showing a 7.0 y/y increase, the highest in 40 years (note here that rising inflation usually leads to a stronger currency as it

fuels rate hike expectations).

The usual suspects are quoted for the lackluster USD performance so far in 2022, such as that Fed rate hikes are already almost fully priced in amid the extended long dollar positioning around the turn of the year. That argument is probably largely correct, as a USD retracement was

much-needed following that strong rally in November.

With the next Fed meeting scheduled for next Wednesday (Jan 26), the broad consolidation will likely continue, though we may already start to see some flows coming back into the dollar, helping it maintain a firmer tone compared to the past two weeks. For instance, the same argument

for positioning may soon start working in the other direction as long positions were probably lightened with the USD decline last week.

The longer-term fundamentals of the Fed being ahead of others in tightening policy remain firmly intact, and investors’ focus should return to this theme sooner or later. Another reason to expect USD firmness to persist over the coming months is an increasingly likely global economic

slowdown (or at least deceleration). Previous instances of synchronized global slowdowns suggest that the US dollar is usually a preferred currency for Fx investors to hold. The Fed rate hikes - which are now a given for this year - can only push the global economy further into deceleration and also increase the USD’s attractiveness from a yield perspective at the same time.

The US economic calendar is light, featuring only 2nd tier data such as the Empire State (Tue) and Philly Fed (Thur) Manufacturing indexes, and housing data (Wed-Thru). Adding to the light trading week will be the fact that there will be no FOMC speakers due to the Fed’s blackout period ten

days before the next meeting.

Euro Fundamental Outlook: Markets May Refocus on ECB Dovishness Amid Light Eurozone Calendar

The euro had a mixed performance in the past week, stronger versus some and weaker versus other currencies. Overall, there is nothing to suggest individual EUR strength at the moment, but rather any gains against selected currencies seem to be part of moves driven by broader stories (such as the USD weakness) unrelated to Europe.

We have a very quiet Eurozone data calendar this week, with only the German ZEW economic sentiment survey on Tuesday, the ECB minutes on Thursday, and a speech by ECB’s Christine Lagarde on Friday worth noting. The markets will carefully look at the ECB minutes for the staff’s thinking

regarding inflation and their QE program, but any surprises are unlikely here as the ECB and President Lagarde have already very clearly communicated their “dovish” stance.

The light calendar means that, much like last week, the EUR will be left to trade on the longer-term macro drivers and global developments. Here the ECB’s dovishness and lagging Eurozone economy will remain in the back of traders’ minds, which should eventually push the currency lower, particularly

versus others with hawkish central banks (e.g., USD, GBP, CAD).

Get my favorite income strategy for 2022 "on the house"

If you are looking for extra income, my Weekly Paycheck program can help. This year alone, people using this strategy have been able to collect an extra $515 of low-risk income each week. Best of all, this works in any market condition--up, down, sideways. I've laid out the exact steps to generate hundreds to thousands of dollars a week in extra income in this free guide.

Get your copy here.

If you have any questions or feedback, don't hesitate to reply to this email.

P.S. Email providers such as Gmail and Yahoo! Mail sometimes place messages in different folders or tabs (often in the promotions tab). To ensure that all trade signals I send will end up in your (primary) inbox folder you can add my email address to your contacts

list.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

|

|

|

|