US Dollar Fundamental Outlook: Careful Fed Approach a Let-Down for USD Bulls

The Fed leaned dovish and slightly disappointed USD bulls at their meeting Wednesday night. Many were expecting Chair Powell to reveal much more details on rate hikes and the plans for tightening, but that didn’t happen. Instead, he urged for “patience on rate hikes,” practically reiterating that rate lift-off won’t necessarily follow

once tapering is completed in summer 2022. The dollar briefly declined on the Fed’s announcement, although it quickly recovered from the dip.

US data was nothing but solid last week. Friday’s Nonfarm Payrolls were better than expected overall, while ISM manufacturing and the ISM services PMIs were also strong and beat the forecasts. The jobs data confirms the positive US economic outlook, but also that the Fed should be in no rush to

tighten policy. It seems USD bulls weren’t impressed with this either, much like with the Fed’s forward guidance two days earlier. Positioning, therefore, likely played a role in pushing the dollar on a retracement. Most importantly, however, the bullish USD dynamics remain completely unchanged following last week’s turbulent schedule of events. Thus, the uptrend should still be very much intact here, and sooner or later, a break to new USD cycle highs is

likely.

The focus on this week’s US calendar is the Wednesday CPI report. Inflation remains the center of attention, and it will be no surprise if this is the event that unlocks further USD gains. As in recent months, if CPI prints higher than expected, it would increase pressure on the Fed to tighten

more quickly and would therefore be bullish for the dollar. Ultimately, the USD uptrend should remain intact even if CPI is a slight miss to forecasts, while a beat could push the USD powerfully higher.

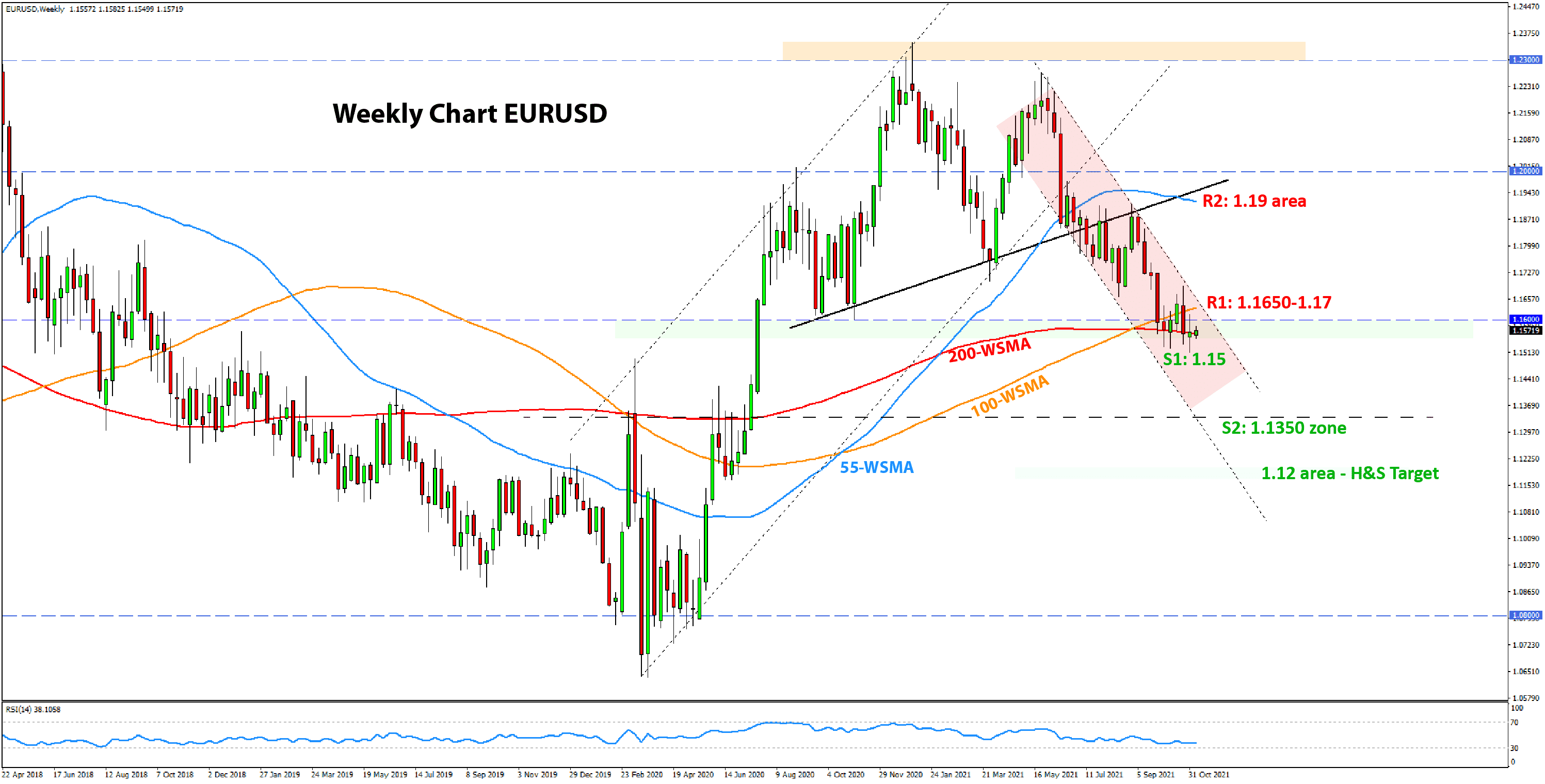

Euro Fundamental Outlook: The Economy is Slowing, the ECB Is Dovish, and Covid Cases Are Surging Again - Not Good for EUR

The euro is kicking off the new trading week near its lows, with the odds favoring a further decline against the likes of the greenback and the commodity dollars (AUD, CAD, NZD).

Eurozone economic data released last week was mostly weak. Notably, German industrial production and retail sales released Friday missed expectations, highlighting the weakness in the economy. Economists are expecting a further deceleration in the

economy.

Covid cases are also surging across the continent and many countries are considering new lockdowns, even ones with very high vaccination rates. This is likely another big negative for the economy that can chop off more points off GDP growth and possibly even cause a technical recession in the

Eurozone.

This calendar for the new week is relatively light, with only the German ZEW economic indicator and the European Commission’s quarterly economic forecasts. If the Commission’s outlook is also weak, it could inspire fresh EUR selling and push the currency on its next bear leg lower.

On balance, the low-yielding EUR with a steady dovish hand from the ECB can find few factors to draw support on. Therefore, it is likely to remain in the group of weak currencies among the Fx majors in the period ahead.