US Dollar Fundamental Outlook: Fed & NFP to Send USD Higher?

The GDP miss and slightly slower than forecasted core PCE inflation did not inflict greater damage to the dollar. In fact, it still ended the week stronger versus all of the major currency pairs but AUD and NZD. This attests to the narrative that the US dollar remains well-positioned for further gains in

the coming weeks.

The Fed meeting this Wednesday and then Nonfarm payrolls on Friday will be the central focus for traders this week and the first huge tests for the bullish USD case. Fed rhetoric since September has turned more hawkish, and the markets now expect them to formally announce QE tapering at this

meeting and potentially give hints about the first interest rate increases in 2022. As we’ve said many times on prior occasions, the Fed is on path to being one of the most hawkish central banks among major Fx currencies, and this is the main theme that should drive the dollar stronger in the period ahead. Furthermore, a potential worsening of risk sentiment in the period ahead could provide an additional boost to the safe-haven dollar, while “risky”

currencies such as NZD, CAD, and AUD may lag, even though their central banks are also hawkish.

A strong Nonfarm payrolls report on Friday will hugely help but is not a prerequisite for further USD gains. Anything close to the 400K NFP and 4.7% unemployment rate forecasts will be enough to keep the USD supported. If the actual figures are much better, the US dollar will likely rally that

much more powerfully. On balance, the probabilities asymmetrically seem to favor the US dollar this week as it would take huge misses in the economic data or a shockingly dovish Fed to reverse the current bullish dynamics.

Other important data on the US calendar are the ISM manufacturing and services PMI reports, which are leading indicators for the economy.

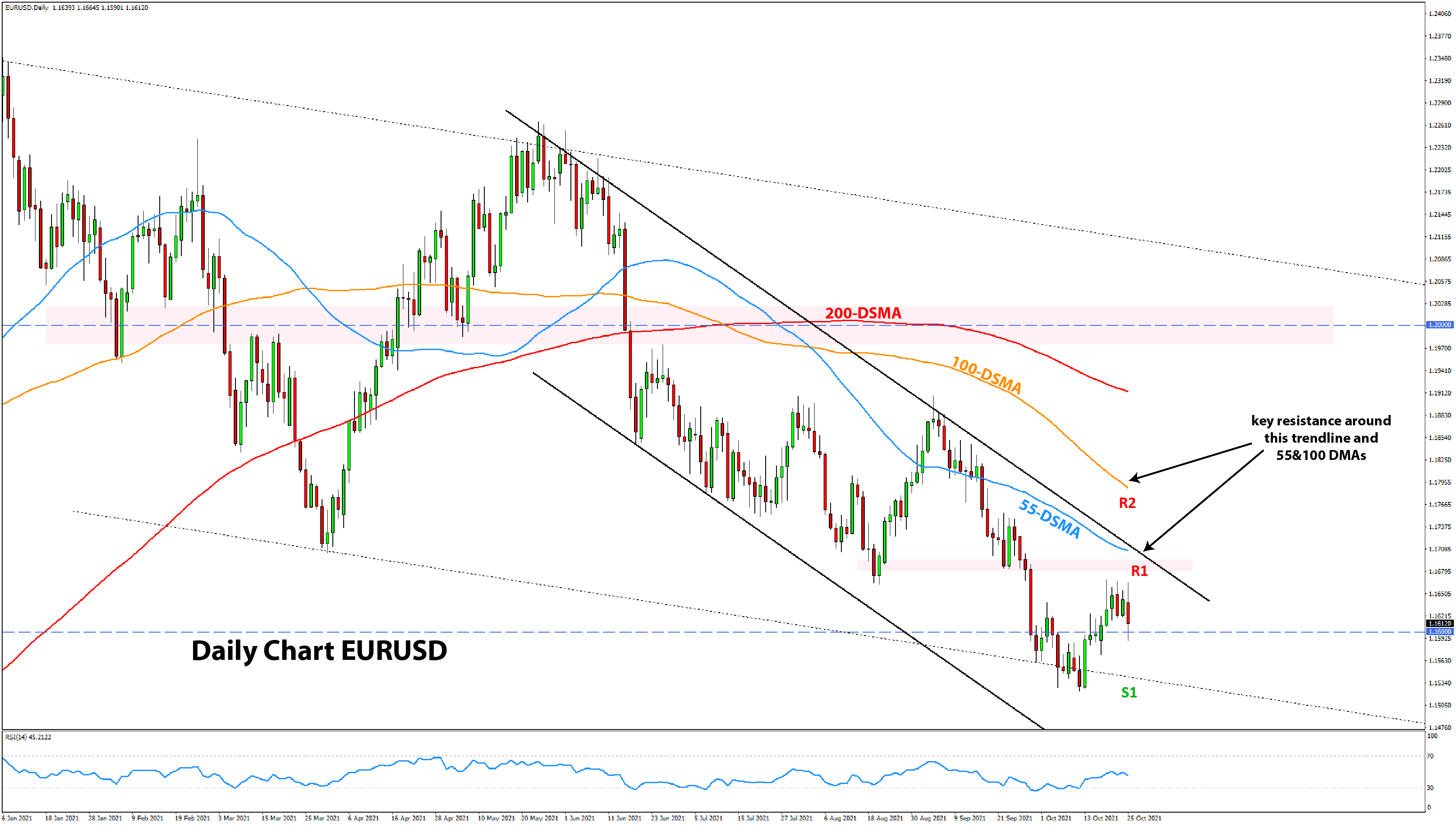

Euro Fundamental Outlook: Excessive EUR Reaction After ECB Rightly Reversed

The EUR jumped higher following the ECB press conference last week, but it was a rally with no solid foundation and hence was rightly fully reversed on the next day. President Lagarde was dovish overall, while the ECB statement contained almost no changes from the previous one from the September meeting. The ECB firmly stays on the view that rising inflation is temporary and will abate next year as these transitory factors subside.

Friday’s Eurozone data was better than expected, but that failed to inspire excitement among EUR traders who sold the currency in anticipation that the economy will weaken further over coming quarters. High commodity prices, especially gas, will undoubtedly hurt growth in Q4 and potentially in Q1 2022.

With this bleak outlook, the ECB has very few reasons to think about tightening policy. Well, at least as long as inflation is “transitory,” right?

The EUR calendar for the week ahead is much sparser compared to last and features only 2nd tier data that won’t move the market. The euro will likely be driven by the larger long-term trend dynamics as well as developments with other currencies and the broader Fx market.