EURUSD, GBPUSD, USDJPY

Weekly Forex Analysis

(December 07 - December 11, 2020)

Hey! This is Philip with our new weekly outlook of the Forex market.

This is only a partial preview of the analysis. Go to the link below to read the Full Weekly Forex Analysis For FREE.

US Dollar Fundamental Outlook: USDX Breaks Lower As Optimism About a Post-Corona Global Recovery Dominates the Mood

Incoming President Joe Biden and his administration choices are starting to take a toll on the dollar. The broad US dollar index (USDX) broke to the lowest levels since April 2018, as investors keep their bearish USD bets at record highs.

Everyone and their mom is bearish on the dollar. A “trade-friendly” Biden coupled with good recovery prospects for 2021 (as we now have COVID vaccines) have the dollar suffer. Investors expect world trade and GDP growth will boom next year. Such an environment facilitates risk appetite and depreciation of the safe-haven US dollar. So, the bearish USD trend is starting to unfold already, and, from the current

perspective, it doesn’t seem like it will stop for the foreseeable future. However, it’s fair to say that the extreme bearish positioning remains a risk for a short squeeze reversal, although it will hardly alter the predominant trend here.

The USD calendar this week features only the CPI print on Thursday. It unlikely that it will affect the underlying USD trend too much, just as last week’s Nonfarm payrolls didn’t. Nonetheless, as noted above, some consolidation in the short-term is possible and would be even healthy after the heavy selling last week.

Euro Fundamental Outlook: Highly-Anticipated ECB Meeting Due on Thursday

This week it is all about the Thursday ECB meeting for the euro. How large will the PEPP quantitative easing will be, and will the ECB mention anything about the strong euro? Those are the main questions on traders’ minds. In September, ECB’s board member Lane verbally intervened as soon as EURUSD reached 1.20 by saying, the EURUSD exchange rate is important for ECB decision making. There haven’t been such comments this

time when EURUSD breached 1.20 last week.

Nonetheless, while the ECB may not like the strengthening euro, there isn’t much they can do aside from “ineffective” verbal intervention. Investors are optimistic that a strong growth rebound will take place next year once the COVID virus is under control. Furthermore, the Biden administration is expected to restore friendly relations with the European Union and even reverse the tariffs that Trump imposed, which would be supportive for the euro

currency.

The EUR price action is telling that a lot of the expected ECB easing is priced in by now. Thus, other than some shallow retracement or consolidation, the uptrends in pairs like EURUSD, EURJPY, and even EURCHF are unlikely to be challenged.

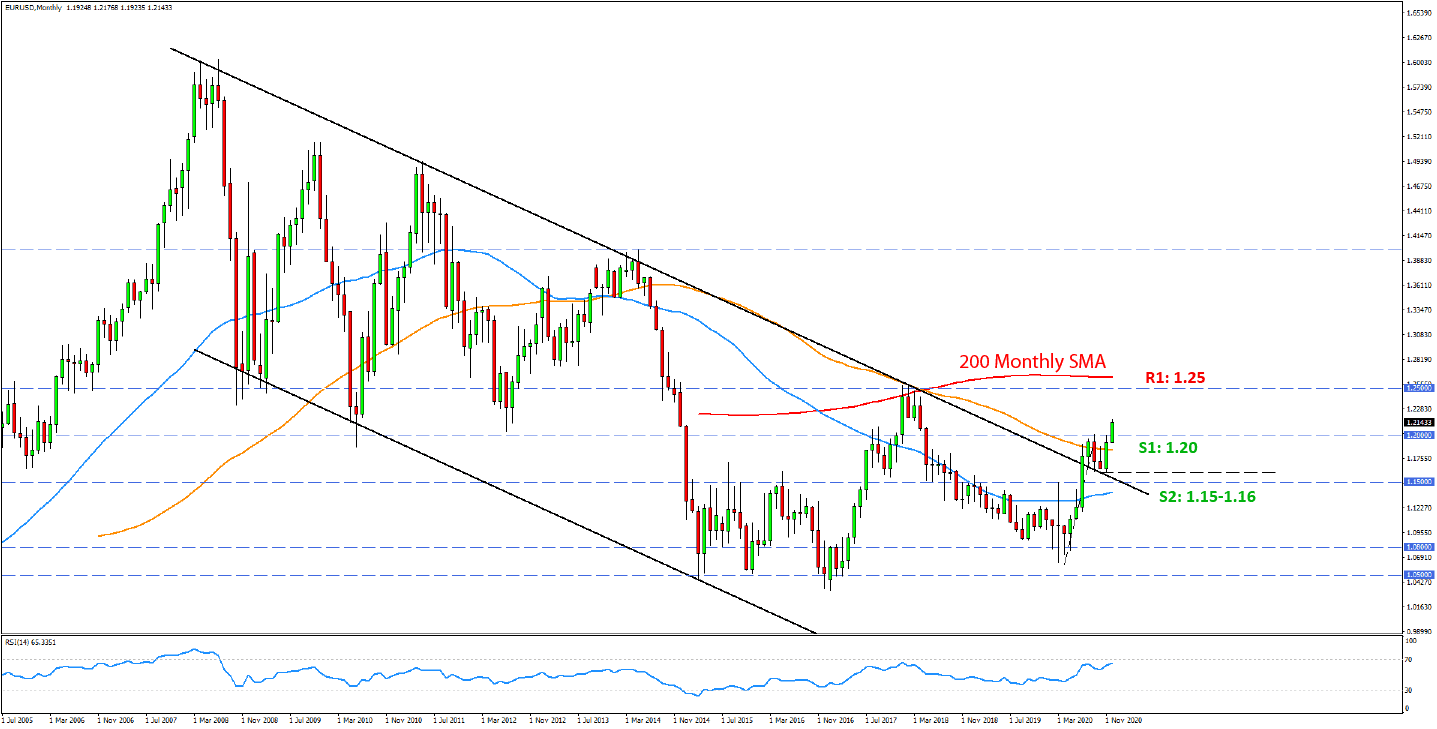

EURUSD Technical Outlook:

This week we are showing the monthly chart to demonstrate the significance of last week’s breakout above 1.20. Namely, the bullish breakout of the 12-year downward channel that occurred in July-August has now been confirmed with this definite move above 1.20. That leaves us to only look up on the monthly chart, with primary target and resistance levels in the 1.25 – 1.27 area. This is also where the 200-period monthly

moving average is located (red line).

To the downside, 1.20 is now likely to act as support if it’s tested again. Below it, the 1.16 lows and the 1.15 zone remain the crucial support zones that should keep this monthly bullish breakout intact.

If you have any questions or feedback, don't hesitate to reply to this email.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

|

|

|

|