EURUSD, GBPUSD, USDJPY

Weekly Forex Analysis

(May 25 - May 29, 2020)

Hey! This is Philip with our new weekly outlook of the Forex market.

This is only a partial preview of the analysis. Go to the link below to read the Full Weekly Forex Analysis For FREE.

US Dollar Fundamental Outlook: USD May Be Back In Demand As US-China Tensions Could Flare-Up Again

The Dollar rebounded on the last two trading days of the past week as US-China tensions may be back on the radar. In addition to the US blaming China for the COVID-19 pandemic, Hong Kong is now returning as another issue between the two countries. US officials stated that the proposed national security laws by the Chinese government would threaten the autonomy of Hong Kong. The US will have to implement further sanctions on both

China and the special administrative region of Hong Kong as well.

While the latest US-China news certainly seems to set the stage for more conflict, traders and investors are already used to this game. Since Trump took office, the tensions have been continuously flipping from on to off between the two great powers, and this could be nothing new. Thus, the initial market reaction so far isn't huge. The Dollar, although rising, remains well within its wider ranges established in early April.

The US economic calendar this week features CB Consumer Confidence, Durable Goods Orders, Preliminary GDP (Second Release), and the PCE Price Index. Unemployment claims are again expected to be above 2 million, which would likely take the US unemployment rate above 20% next month.

Euro Fundamental Outlook: EUR Stronger On Franco-German Proposal For 500 Bln Recovery Fund

The Franco-German proposal for a 500 billion euros recovery program was received well by the markets, and the euro rallied in response last week. If accepted, the plan would allow the EU borrowings of up to 500 billion euros to aid the countries and sectors most hit by the coronavirus pandemic.

On the other hand, however, there will undoubtedly be opposition to this proposal from some EU countries, so it's still early to say that this is a done deal. Furthermore, there is still the issue of the German court ruling on the ECB QE program, asking the central bank to prove it hasn't overstepped its mandate or else lose Germany as a participant in the bond purchases. So overall, downside political risks to the EUR currency remain alive, but

the 500 billion fund proposed last week by Germany and France is an encouraging sign for euro bulls.

The better than expected PMI reports last week also helped the euro to gain some ground. In the current week, the main focus will be on Friday's Flash CPI Inflation data for the Eurozone. The German Ifo index was released earlier today and showed business conditions improved stronger than forecasted over the previous month.

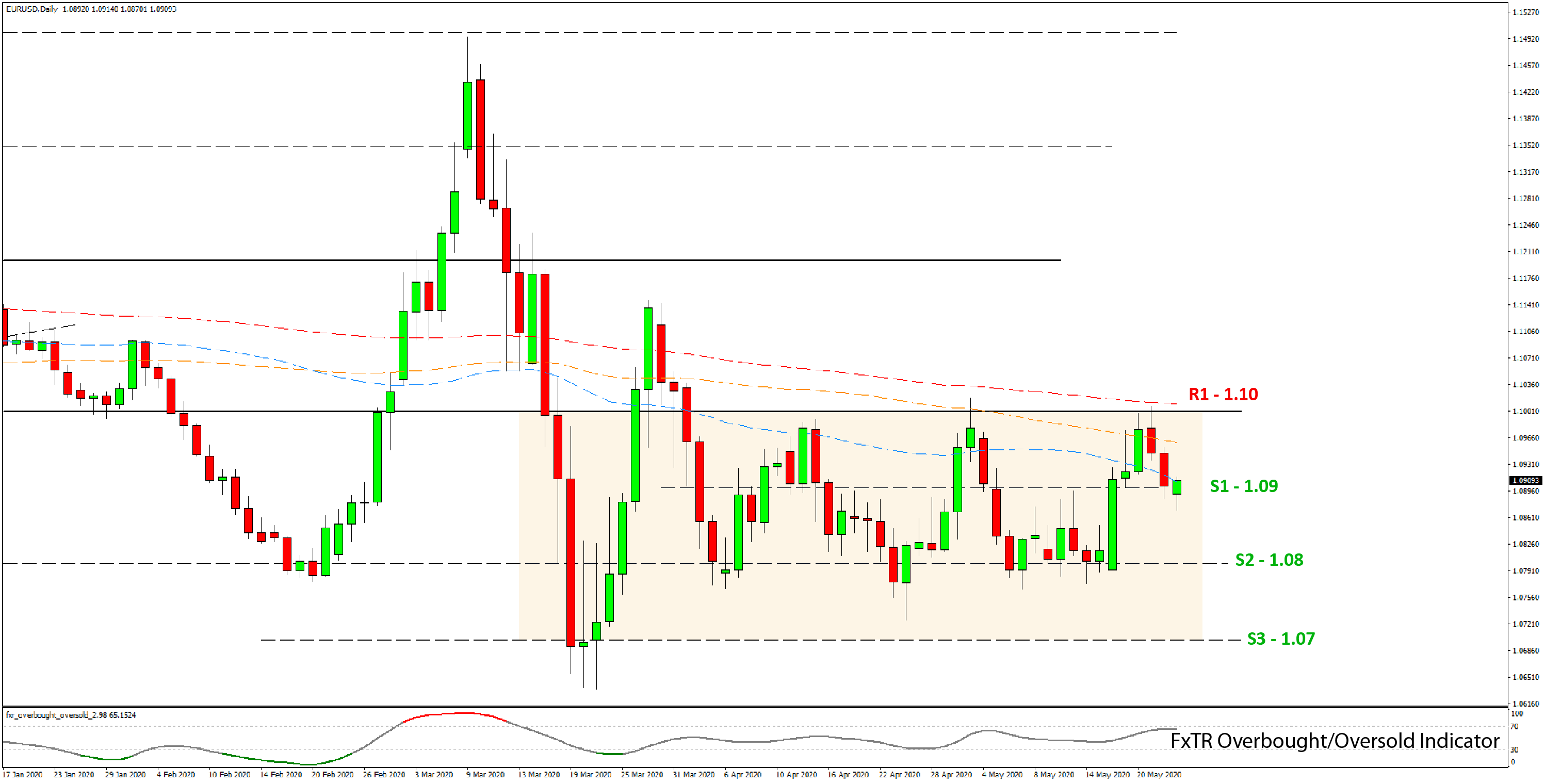

EURUSD Technical Outlook:

If EURUSD was at the bottom of the range this time last week, now it is in the middle of the sideways market action after having tested the 1.10 top of the range and reversed there.

If the sideways price action continues, then EURUSD could test the 1.08 support again over the coming days. The mid-point of the range, the 1.09 zone, is also a technical area, and as we can see, EURUSD is reacting there.

The upside seems capped at the solid 1.10 resistance for now. A breakout in either direction could get things moving here, but there is nothing promising of that sort for the moment.

If you have any questions or feedback, don't hesitate to reply to this email.

High Risk Warning: Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Any opinions, news, research, predictions, analyses, prices or other information contained in this newsletter is provided as general market commentary and does not constitute investment advice. FX Trading Revolution will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

|

|

|

|